The world changed in March, as the stock market tanked and the U.S. economy screeched to a halt in response to the coronavirus pandemic. Amid continued lockdowns and a spike in unemployment to more than 30 million by late April, many Americans wondered if they would ever be able to retire.

Many younger and mid-career workers who were lucky enough to hold on to their jobs during the downturn may benefit from lower stock valuations as they dollar-cost-average their retirement savings over the coming years and decades. It’s new retirees and people nearing retirement who face the greatest threat. Sequence-of-return risk — being forced to sell depressed assets in a down market to finance their spending if they don’t have enough cash to weather the storm — could be devastating to their long-term financial security.

“If you are trying to meet a spending goal and assets are losing value, you have to withdraw a higher percentage from your portfolio,” said Wade Pfau, retirement income researcher and professor of retirement income at The American College for Financial Services.

Advertisement

“Unless investment returns earn at least as much as the withdrawal rate, the portfolio will spiral downward,” Pfau said. “Those first five to 10 years of retirement really drive about 80% of the outcome.”

That means new retirees who are relying solely on their investments for income may need to spend less now to make sure they don’t run out of money later.

The traditional 4% rule, which says retirees can safely withdraw 4% of their nest egg during the first year of retirement and subsequently increase their annual withdrawals by the rate of inflation over a 30-year retirement without running out of money, no longer applies, Pfau said.

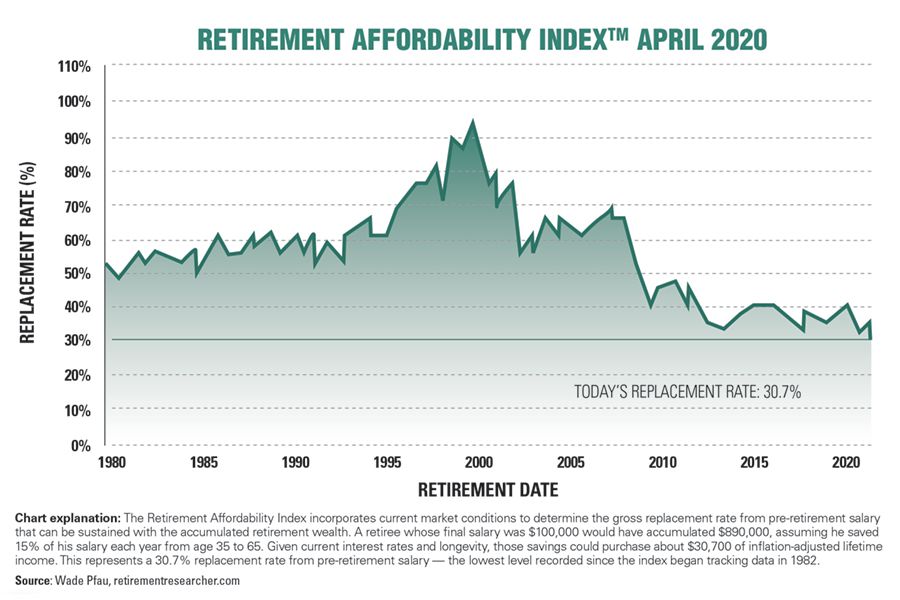

Given the record-low interest rates and the severe market volatility, returns from a diversified portfolio are lower now than when the 4% rule was established 25 years ago, he said. For a couple who both turn 65 today, the safe withdrawal rate from a diversified portfolio with at least a 50% stock allocation is closer to 2.29%, Pfau said. Consequently, his proprietary Retirement Affordability Index reached its lowest level ever last month.

Lower overall returns also mean pre-retirees would need to save more money to support the same desired level of spending in retirement at the lower safe withdrawal rate. For example, using the 4% rule, retirees could withdraw $40,000 from a $1 million portfolio, but they would need a $1.75 million portfolio to support the same spending level at a 2.29% withdrawal rate.

David Blanchett, head of retirement research at Morningstar Inc., thinks Pfau’s estimate is too low. Assuming a retiree has no other source of guaranteed income, Blanchett thinks today’s safe withdrawal rate is about 3%. “But in reality, most Americans get at least half of their income from Social Security,” he said.

“These models assume that you withdraw the same amount of money each year, increased for inflation,” Blanchett added. “In reality, you might have to cut back your spending. But even a 3% withdrawal rate could be overly conservative for a retiree who has other sources of guaranteed lifetime income from Social Security, a pension and perhaps an annuity.”

BEYOND TRADITIONAL INVESTMENTS

For many retiring clients, such a measly withdrawal rate won’t be enough to live on. Consequently, financial advisers may need to look beyond traditional investments and consider all of a household’s assets to generate sufficient income. The goal should be to create a safe, inflation-protected income floor (if there is no employer-provided pension) that in combination with Social Security will cover essential expenses throughout retirement. Once the essentials are covered, invested assets can be positioned for growth to fund discretionary expenses and other financial goals.

For those nearing retirement, the nationwide stay-at-home orders during the pandemic may provide an excellent opportunity to practice retirement. With nowhere to go and few opportunities to spend money on discretionary expenses like restaurants, travel and live entertainment, it becomes abundantly clear which expenses are essential and which costs fall into the wants-but-not-needs category.

TOTAL HOUSEHOLD ASSETS

“Consider all assets and liabilities on a household’s balance sheet,” Pfau said.

“The best strategies are not investment-only or insurance-only,” he explained. “Together these approaches can fund different goals with different risk levels and trade-offs.”

Such comprehensive retirement income strategies might include buying annuities to transfer some of the client’s market risk to an insurance company in exchange for guaranteed income; tapping home equity through a home equity line of credit or reverse mortgage to fund income needs without selling investments at a loss; or taking tax-free withdrawals from an existing cash-value life insurance policy or selling an insurance policy through a life settlement to serve as a temporary income bridge.

“By incorporating partial annuity use, having access to a buffer asset [such as a reverse mortgage or cash-value life insurance] and having some capacity to reduce spending, a reasonable withdrawal rate can still be possible and can provide some relief to those approaching retirement age at this unprecedented time,” Pfau said.

WORK LONGER

For clients who are on the verge of retirement, working longer may be the best solution to surviving the current downturn, said Chip Munn, head of Signature Wealth Strategies and author of “The Retirement Remix.”

“Still having earned income, even on a scaled-back basis, allows you to weather difficult times,” Munn said. Having some earnings coming in enables clients to defer drawing down on their retirement assets in a volatile market and put off claiming Social Security to create a bigger guaranteed benefit in the future.

The value of the 8% per year delayed retirement credit for every year an individual postpones claiming Social Security beyond full retirement age up to age 70 is more compelling than ever in today’s zero-interest-rate environment — for those who can afford to wait.

Blanchett agreed on the value of working longer and delaying Social Security. “The lower interest rates go, the more attractive Social Security is from a pure investment position,” he said. “It’s better to delay Social Security, which is linked to inflation and guaranteed for life.”

But Munn does not subscribe to the work-until-you-die philosophy. Quite the opposite. “The imbalance of work and play makes Americans slaves to work, fear, declining health and decreased happiness,” he said. Instead, most clients would be better off enjoying their vacation days and pursuing their passions during their working years and gradually reducing their workload, rather than retiring completely. Working just a few years longer can substantially improve retirement prospects.

One of the silver linings of the stay-at-home orders during the pandemic may be that both employers and employees reevaluate the future of work and retirement. “Employers could retain human capital and employees could have a longer career arc,” Munn said. “A lot of people are rethinking their priorities and what they want their life to look like.”

FORCED RETIREMENT

Not everyone gets to decide when — or if — to retire. Some of the tens of millions of people who lost their jobs during the steepest economic downturns in history may never work again. For the newly unemployed who are at least 62 years old, filing for Social Security may be necessary even if claiming benefits before full retirement age can result in a permanent reduction in monthly payments.

An uptick in individuals claiming Social Security benefits at the earliest possible age of 62 as a result of the COVID pandemic would reverse a nearly 20-year trend of workers claiming benefits at older ages. The percentage of men who claimed benefits at 62 dropped from 40% in 2000 to 22% in 2018, and early claims for women dropped from 44% in 2000 to 25% in 2018, according to the Social Security Administration.

However, claiming reduced Social Security benefits may not be enough to support clients’ income needs, particularly if they are unwilling to cash in retirement assets in a down market. Consequently, financial advisers may need to look beyond investible assets and explore other ways to generate income.

“Incorporating home equity through reverse mortgages can be an effective risk management tool during times of extreme market volatility,” said Steve Resch, a financial adviser and vice president of retirement strategies at Finance of America Reverse, one of the nation’s largest reverse mortgage lenders. Senior housing wealth reached an all-time high of $7.23 trillion in April, according to the National Reverse Mortgage Lenders Association quarterly index.

A reverse mortgage lets homeowners who are 62 or older borrow against the equity in their homes as long as they live there. It can help clients stay invested during the current stock market lows while creating an alternative income stream to ensure there is cash available to pay bills and address other important financial needs, such as paying off an existing mortgage to lower monthly expenses.

There are some steep upfront costs — including a mandatory 2% insurance fee based on the value of the home up to Federal Housing Administration lending limits — but those can be wrapped into the cost of the loan, and no repayments are required as long as the borrower or his or her spouse live in the home.

“People are losing their jobs and they have an asset they can draw on without having to drain their investments,” Resch said. “It is a message we have been talking about for years, and it seems to be coming home to roost.”

The Coronavirus and Your Retirement: In the latest episode of her podcast, Mary Beth Franklin speaks with Tom Wald of Transamerica about how the coronavirus pandemic has affected our economy, our investments, and our everyday lives.